Investor anticipation for a Federal Reserve interest rate cut has surged following weaker-than-expected U.S. labor data and significant leadership changes within the Federal Open Market Committee.

As the new week begins, confidence among investors for a cut in the base interest rate by the Federal Reserve has grown substantially. This comes after the latest U.S. labor data revealed a notable shortfall, with July’s payroll growth at just 73,000 compared to forecasts of around 100,000. Additionally, previous figures for May and June have been significantly revised down, suggesting deeper vulnerability in the job market. The probability of a rate cut in September now stands at 87%, influenced further by the resignation of FOMC member Adriana Kugler, potentially paving the way for a more dovish trajectory at the Fed.

Until the data revision, analysts were doubtful that the Federal Reserve would opt for an interest rate cut. However, the recent adjustments to the employment numbers have shifted many to speculate that a rate reduction might be on the table, particularly aligning with President Trump’s calls for cheaper money to stimulate economic activity amidst labor market concerns.

The Labor Department’s report last Friday not only highlighted July’s underwhelming payroll numbers but also included downward revisions totaling a reduction of 258,000 for May and June. This disclosure has ignited discussions on the frail state of the labor market, where the three-month average gain now rests at 35,000, a stark sign of potential economic fragility.

In response to these revisions, President Trump dismissed Erika McEntarfer, the Bureau of Labor Statistics commissioner, expressing dissatisfaction over the mishandling of employment statistics. As investors come to grips with these developments, attention also veers towards upcoming trade-related volatility, given Trump’s tariff deadline set for August 7.

Kugler’s resignation from the FOMC provides President Trump an opportunity to appoint a new member who might be sympathetic to his stance on lowering the base rate. This possibility increases optimism among analysts hoping for a path towards interest rate normalization.

Before the New York markets opened this week, the market atmosphere reflected investor sentiments: the S&P 500 had closed down 1.6%, and the Nasdaq was down 2.24% last Friday. Across the Atlantic, London’s FTSE 100 rose 0.3%, and Germany’s DAX rose 1.1%. However, S&P futures indicated a 0.65% rise, pointing to some investors buying the dip.

In Asia, where expectations for imminent trade deals with China or India remain dim, Japan’s Nikkei 225 decreased by 1.25%, while India’s Nifty 50 saw an increase of 0.65%. Anticipations build around September when many analysts expect Fed Chairman Jerome Powell to announce a rate cut, potentially hinting at such a shift during the forthcoming Jackson Hole Symposium.

The volume of trading in the CME’s 30-Day Federal Funds futures and options dramatically increased between July 31 and August 1, driven by the altered labor data, indicating a strong expectation for a base rate drop to around 3.75%, equivalent to two cuts by the Fed. Markets are pricing in more cuts by the end of the year.

The economic outlook’s unexpected downgrade was not the ideal scenario for rate cuts, as investors had hoped for stable inflation levels to encourage such moves. Nonetheless, some, like Deutsche Bank’s Jim Reid, point out the Fed’s potential to pivot given the recent changes in key personnel and economic data. He highlights the increased probability of a rate cut as Fed members may reassess their positions in light of the revised payroll data.

Reid further suggested that the current scenario offers President Trump a chance to appoint a dovish member to the Fed, possibly aligning with his economic agenda. Present member dissenters, who were Trump appointees, contribute to the conversation surrounding potential shifts within the Fed’s approach.

Alongside these developments, Macquarie analysts now anticipate a swifter timeline for interest rate cuts, tying their predictions directly to the labor market’s latest performance. David Doyle from Macquarie notes that while September’s cut chances have risen, the decision lies with future employment and inflation data developments.

Fed Chairman Jerome Powell had previously underscored the importance of maintaining a delicate balance between inflation and employment. He remarked on the need for attentiveness to potential risks in employment while promising that upcoming data would better inform the Fed’s future monetary policy.

In contrast, Bernard Yaros from Oxford Economics remains cautious in reevaluating the company’s forecast, suggesting that the recent labor report poses challenges, yet is not conclusive enough to forecast immediate rate cuts.

The market activity before the New York opening bell reflected a mixed but upward tilt: S&P 500 futures were up 0.7% premarket, Europe’s STOXX 600 alongside the FTSE 100 and China’s CSI 300 showed gains, while Japan’s Nikkei 225 faced declines. Bitcoin remained stable at approximately $114,551.

This information outlines the economic landscape as shaped by recent labor data and emerging monetary policy expectations.

Source: Original article

Luxury Jewelry is well-known for its sophisticated designs and utilization of the most precious and uncommon unrefined substances. The Luxury Jewelry Market is vigorous and quickly developing. It’s also exceptionally divided and determined by buyer conduct and style. In the nearing years, huge market development is normal, from increasing extra cash and amplifying buyer consumption of extravagant merchandise. Assimilating the luxury gems industry with diversion and allure businesses has set new open doors for the market.

Luxury Jewelry is well-known for its sophisticated designs and utilization of the most precious and uncommon unrefined substances. The Luxury Jewelry Market is vigorous and quickly developing. It’s also exceptionally divided and determined by buyer conduct and style. In the nearing years, huge market development is normal, from increasing extra cash and amplifying buyer consumption of extravagant merchandise. Assimilating the luxury gems industry with diversion and allure businesses has set new open doors for the market.

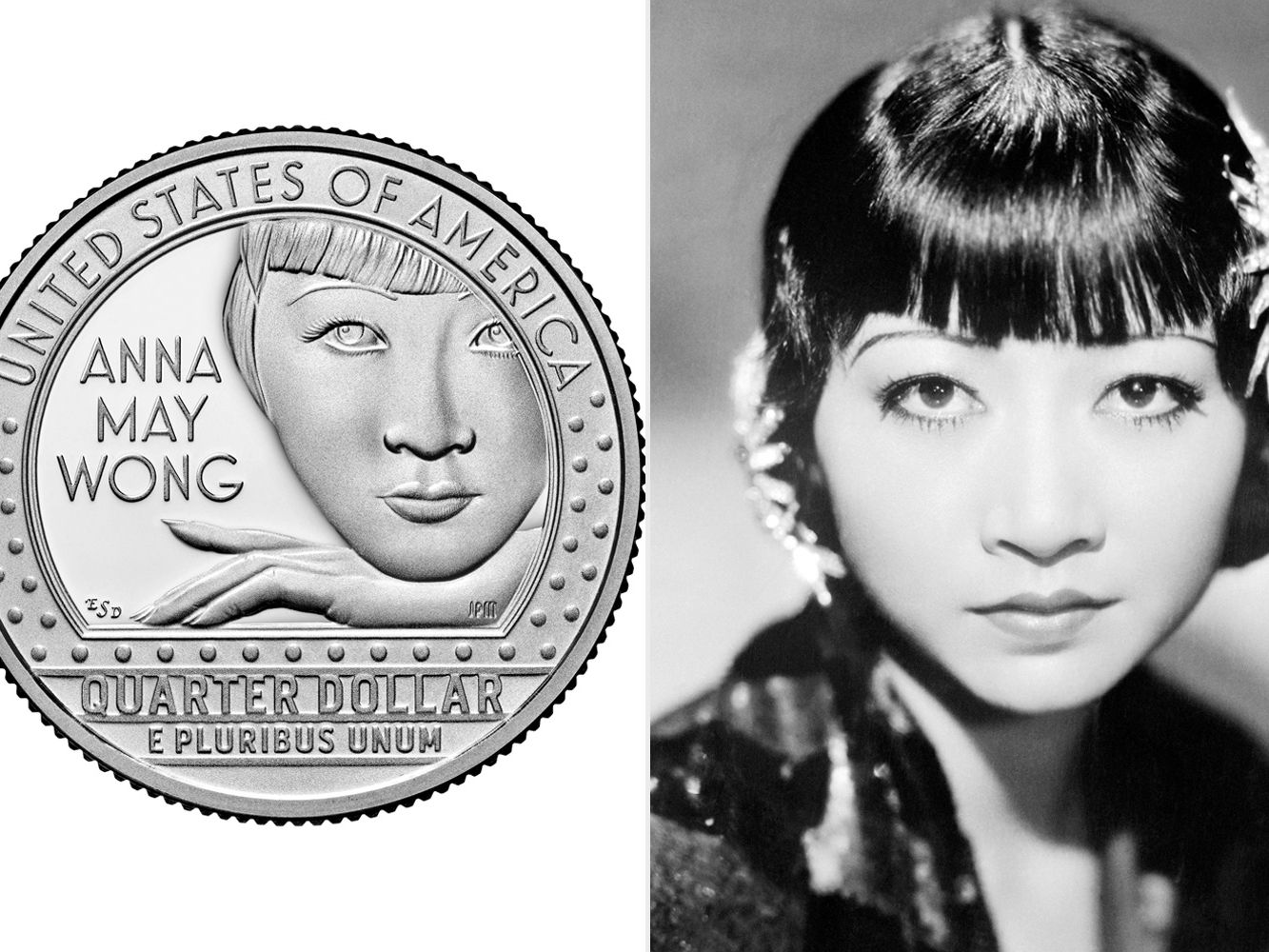

Born in Los Angeles, she began acting at 14 and took a lead role in “The Toll of the Sea” three years later, in 1922. She went on to appear in dozens of movies but faced deeply entrenched racism in Hollywood, where she struggled to break from stereotypical roles.

Born in Los Angeles, she began acting at 14 and took a lead role in “The Toll of the Sea” three years later, in 1922. She went on to appear in dozens of movies but faced deeply entrenched racism in Hollywood, where she struggled to break from stereotypical roles.

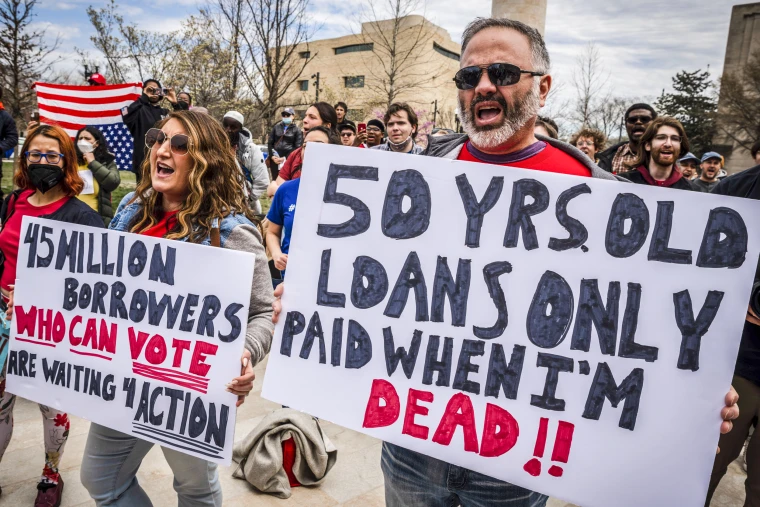

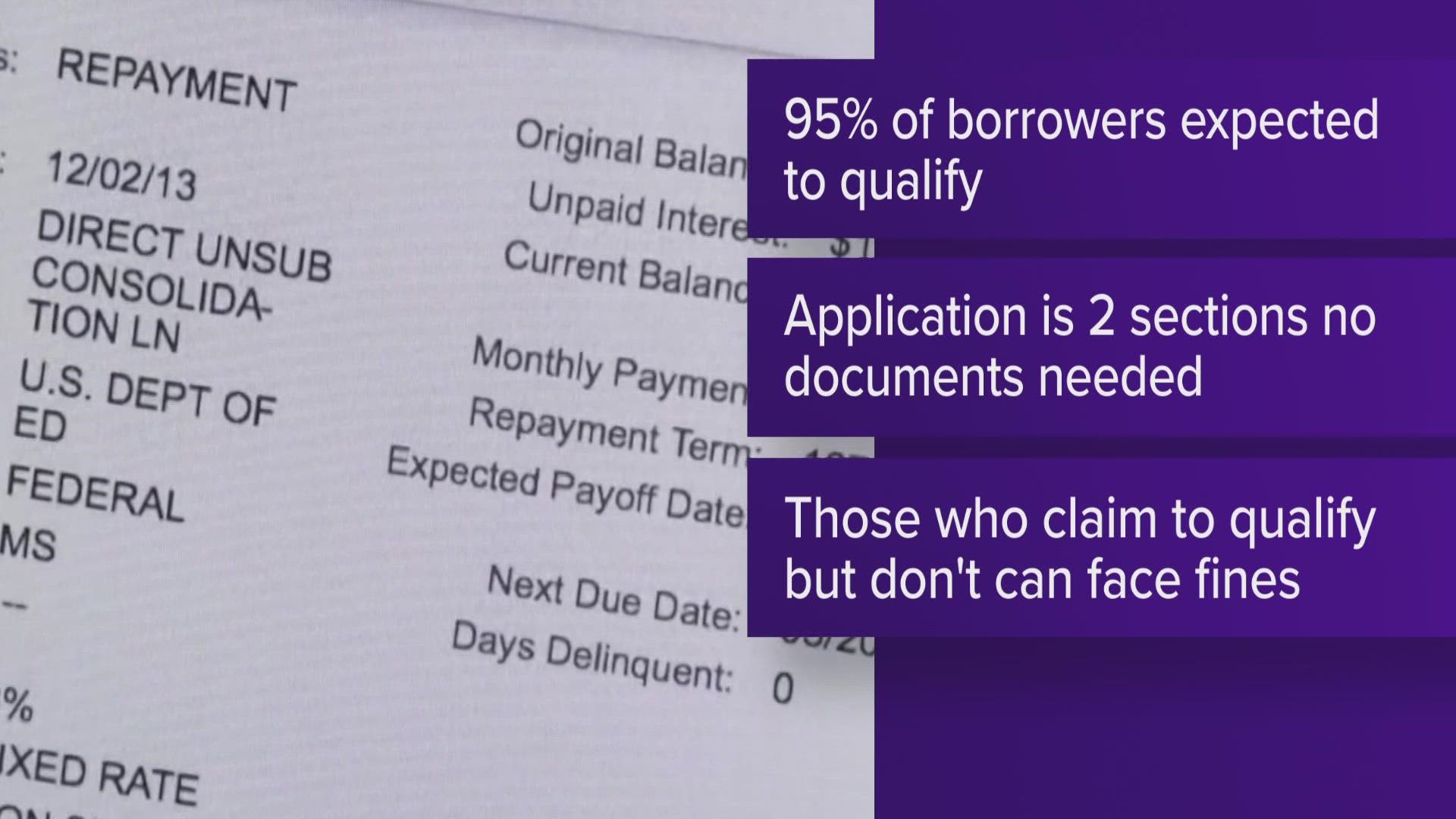

The Education Department’s technical team will be responding to potential issues in real-time, and although the application itself won’t change, the team may make changes to the website if faced with any glitches.

The Education Department’s technical team will be responding to potential issues in real-time, and although the application itself won’t change, the team may make changes to the website if faced with any glitches.