(AP) — The United States Supreme Court won’t have far to look if it wants a personal take on the “crushing weight” of student debt that underlies the Biden administration’s college loan forgiveness plan. Justice Clarence Thomas was in his mid-40s and in his third year on the nation’s highest court when he paid off the last of his debt from his time at Yale Law School.

Thomas, the court’s longest-serving justice and staunchest conservative, has been skeptical of other Biden administration initiatives. And when the Supreme Court hears arguments Tuesday involving President Joe Biden’s debt relief plan that would wipe away up to $20,000 in outstanding student loans, Thomas is not likely to be a vote in the administration’s favor.

But the justices’ own experiences can be relevant in how they approach a case, and alone among them, Thomas has written about the role student loans played in his financial struggles.

A fellow law school student even suggested Thomas declare bankruptcy after graduating “to get out from under the crushing weight of all my student loans,” the justice wrote in his best-selling 2007 memoir, “My Grandfather’s Son.” He rejected the idea.

It’s not clear that any of the other justices borrowed money to attend college or law school or have done so for their children’s educations. Some justices grew up in relative wealth. Others reported they had scholarships to pay their way to some of the country’s most expensive private institutions.

Of the seven justices on the court who are parents, four have signaled through their investments that they don’t want their own children to be saddled with onerous college debt, and have piled money into tax-free college savings accounts that might limit any need for loans.

Chief Justice John Roberts and Justice Neil Gorsuch have the most on hand, at least $600,000 and at least $300,000, respectively, according to annual disclosure reports the justices filed in 2022. Each has two children.

Justices Amy Coney Barrett, who has seven children, and Ketanji Brown Jackson, who has two, also have invested money in college-savings accounts, in which any earnings or growth is tax free if spent on education. None of the justices would comment for this story, a court spokeswoman said.

Thomas wrote vividly about his past money woes in his up-from-poverty story, recounting how a bank once foreclosed on one of his loans because repayment and delinquency notices were sent to his grandparents’ house in Savannah, Georgia, instead of Thomas’ home at the time in Jefferson City, Missouri.

Thomas was able to take out another loan to repay the bank only because his mentor, John Danforth, then-Missouri attorney general and later a U.S. senator, vouched for him.

Thomas noted that he signed up for a tuition postponement program at Yale in which a group of students jointly paid for their outstanding loans according to their financial ability, with those earning the most paying the most.

At the time, Thomas’ first wife, Kathy, was pregnant. “I didn’t know what else to do, so I signed on the dotted line, and spent the next two decades paying off the money I borrowed during my last two years at Yale,” Thomas wrote.

When he was first nominated to be a federal judge in 1989, Thomas reported $10,000 in outstanding student loans, according to a news report at the time. The Biden administration has picked the same number as the amount of debt relief most borrowers would get under its plan.

Personal experience can shape the justices’ questions in the courtroom and affect their private conversations about a case, even if it doesn’t figure in the outcome.

“It is helpful to have people with life experiences that are varied just because it enriches the conversation,” Justice Sonia Sotomayor has said. Sotomayor, like Thomas, also grew up poor. She got a full scholarship to Princeton as an undergraduate, she has said, and went on to Yale for law school, as Thomas did.

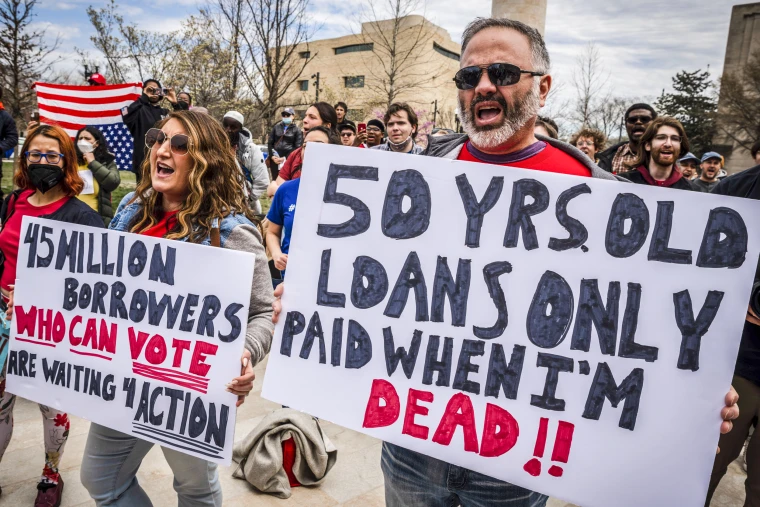

Keeping people from avoiding the kinds of difficult choices Thomas faced is a key part of the administration’s argument for loan forgiveness. The administration says that without additional help, many borrowers will fall behind on their payments once a hold in place since the start of the coronavirus pandemic three years ago is lifted, no later than this summer.

Under a plan announced in August but so far blocked by federal courts, $10,000 in federal loans would be canceled for people making less than $125,000 or for households with less than $250,000 in income. Recipients of Pell Grants, who tend to have fewer financial resources, would get an additional $10,000 in debt forgiven.

The White House says 26 million people already have applied and 16 million have been approved for relief. The program is estimated to cost $400 billion over the next three decades.

The legal fight could turn on any of several elements, including whether the Republican-led states and individuals suing over the plan have legal standing to go to court and whether Biden has the authority under federal law for so extensive a loan forgiveness program.

Nebraska and other states challenging the program argue that far from falling behind, 20 million borrowers would get a “windfall” because their entire student debt would be erased, Nebraska Attorney General Michael Hilgers wrote in the states’ main Supreme Court brief.

Which of those arguments resonate with the court may become clear on Tuesday.

When she was dean of Harvard Law School, Justice Elena Kagan showed her own concern about the high cost of law school, especially for students who were considering lower-paying jobs.

Kagan established a program that would allow students to attend their final year tuition-free if they agreed to a five-year commitment to work in the public sector. While that program no longer exists, Harvard offers grants to students for public service work.

At the time the program was created, Kagan said she wanted students to be able to go to work where they “can make the biggest difference, but that isn’t the case now.” Instead, she said: “They often go to work where they don’t want to work because of the debt burden.”