Wall Street faced a significant sell-off as the Federal Reserve maintained interest rates, revealing internal divisions over inflation management and raising concerns about capital expenditures in artificial intelligence.

Wall Street experienced a steep sell-off on Wednesday after the Federal Reserve voted 9–3 to keep the benchmark interest rate target steady at 3.50% to 3.75%. This decision defied the three dissenting policymakers who advocated for an immediate rate increase to combat ongoing inflation. Investor sentiment was further dampened by rising concerns over the substantial capital expenditures required for artificial intelligence development. Notably, Meta Platforms revised its 2026 spending outlook upward to as much as $145 billion. The tech-heavy Nasdaq 100 index fell by 2.1%, marking an 11% cumulative drop from its June record peak as markets reevaluated whether massive AI infrastructure investments would yield near-term cash flow. Despite strong projected second-quarter earnings growth across the broader S&P 500, major indices ended significantly lower, reflecting widespread portfolio rebalancing amid heavy trading volume. With global oil prices surging and disinflation progress stalling above the central bank’s target, analysts now anticipate increasing pressure on the Fed to enact a rate hike at its upcoming September policy meeting.

Major U.S. stock indices closed sharply lower on Wednesday following the Federal Reserve’s decision to maintain its benchmark interest rate target at 3.50% to 3.75%. This marks the fifth consecutive meeting without a rate adjustment as central bankers grapple with persistent inflationary pressures. The policy decision was characterized by significant internal disagreement, with three members of the Federal Open Market Committee dissenting in favor of an immediate rate hike amid rising geopolitical energy shocks and elevated corporate capital spending. Financial markets reacted with broad-based declines, driven by growing investor skepticism regarding heavy capital expenditures in artificial intelligence infrastructure, shifting rate expectation timelines, and broader macroeconomic uncertainty.

The Federal Reserve’s Federal Open Market Committee (FOMC) concluded its two-day policy review on Wednesday by keeping the federal funds target rate unchanged in the 3.50% to 3.75% range. While this outcome was broadly anticipated by financial markets, the vote highlighted a deepening divide among monetary authorities over how aggressively to address inflation that has remained above the central bank’s 2% annual target for over five years.

The 9–3 decision featured formal dissents from Cleveland Fed President Beth Hammack, Minneapolis Fed President Neel Kashkari, and Dallas Fed President Lorie Logan, all of whom advocated for a 25-basis-point interest rate increase. These officials expressed concern that price pressures are stalling well above preferred levels, exacerbated by energy price volatility linked to ongoing conflicts in the Middle East, foreign trade tariffs, and substantial private-sector demand for data center capacity and power infrastructure.

During a post-meeting press conference at the Federal Reserve building in Washington, Fed Chair Kevin Warsh addressed reporters with a deliberate and calm demeanor, emphasizing the central bank’s unwavering focus despite market volatility. He reiterated that the Fed maintains no implicit tolerance for elevated price indexes.

“For some households, businesses, and market professionals, five years of high inflation have left a mistaken impression that is hard to shake: that the Fed’s implicit inflation target was somehow above 2 percent,” Warsh stated, looking directly at the audience. “Let me reiterate: There is no soft inflation target, there is no soft implicit target — not on this Committee’s watch. There is only a target, and it is 2 percent. Not one of my FOMC colleagues is under any illusion.”

Warsh acknowledged that corporate investment in technology and artificial intelligence is laying critical groundwork for future economic productivity, though he also recognized that rapid capital accumulation presents unique challenges for monetary policy.

“The Fed held pat, as expected. The bigger question now though becomes, how much pressure will they have to hike in September?” noted Ryan Detrick, chief market strategist at Carson Group. “Inflation is running hot, and with surging crude oil, the market expects the next hike to indeed be in September.”

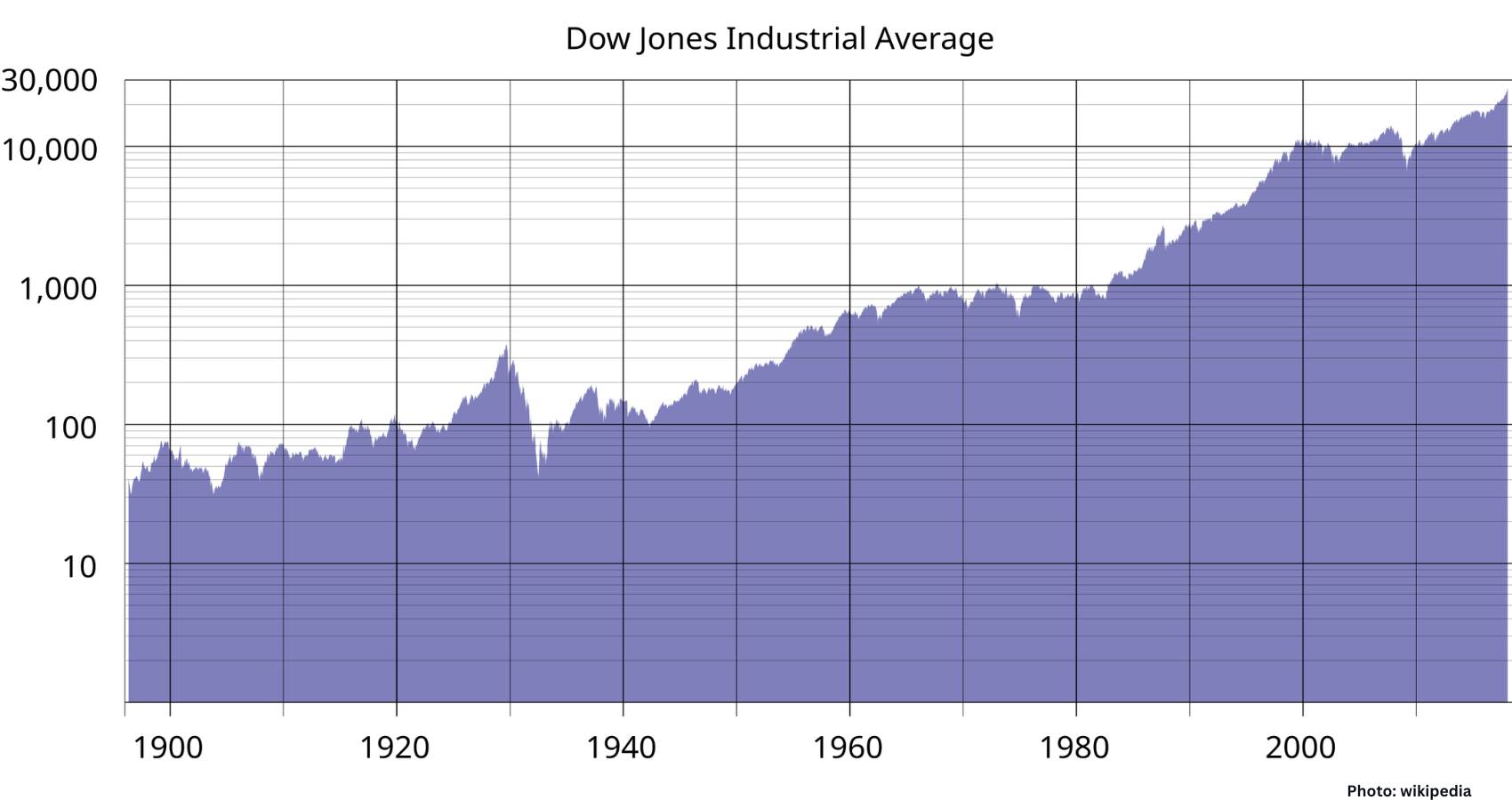

Equities posted substantial losses across all three major market benchmarks following the policy statement and subsequent press briefing. The benchmark S&P 500 index dropped 1.52%, or 112.80 points, to close at 7,316.15 points, marking its lowest closing level in a month. The Dow Jones Industrial Average slid 2.19% to finish at 51,594.14 points, while the tech-heavy Nasdaq Composite Index declined 1.74% to end at 24,442.94 points.

Market breadth was decisively negative across Wall Street. Within the S&P 500, declining issues outpaced advancing ones by a 1.8-to-1 ratio. Eight of the 11 primary S&P 500 sector groups posted negative returns, led by a 3.24% fall in industrial equities and a 2.50% drop in information technology stocks. Across the S&P 500, 32 securities reached new 52-week highs while four registered new lows; on the Nasdaq, 121 stocks recorded new highs against 230 establishing new lows.

Trading activity was robust across domestic trading venues, with total volume reaching 17.7 billion shares, exceeding the 20-day moving average of 17.3 billion shares. This surge reflects heightened institutional portfolio realignments following the rate decision.

A primary driver of Wednesday’s downward market pressure was a pronounced retrenchment in artificial intelligence and semiconductor equities. The Nasdaq 100 index, which comprises the 100 largest non-financial enterprises listed on the exchange, fell 2.1% during regular session hours, now retreating approximately 11% from its record high established in June and entering formal correction territory.

Investors have expressed growing concern regarding the escalating capital expenditure plans of major technology companies. Market participants are questioning whether the hundreds of billions of dollars allocated to AI chips, server architecture, and energy supply arrangements will generate near-term free cash flow commensurate with current valuation multiples.

These anxieties were evident in extended trading session activity. Shares of Meta Platforms fell 4% after the social media giant revised its full-year 2026 capital expenditure guidance upward to a range of $130 billion to $145 billion, compared to its previous projection of $125 billion to $145 billion. Conversely, Microsoft shares edged up 0.6% in post-market trading after reporting quarterly cloud infrastructure revenue growth that exceeded analyst projections, providing a counter-example of monetization progress.

“Investors worry that major U.S. companies are deepening a web of AI-linked investments and continuing to funnel billions into the emerging technology at the expense of free cash flow,” observed market equity analysts following the releases.

Despite the day’s broad equity declines, corporate earnings fundamentals remain relatively robust. Analysts surveyed by LSEG I/B/E/S anticipate aggregate second-quarter earnings for S&P 500 companies to expand by 40% year-over-year, with hardware, cloud computing, and AI-adjacent enterprises accounting for the majority of that growth. Following recent pullbacks, the S&P 500 is trading at approximately 20 times forward earnings expectations, slightly above its 10-year historical average of 19 times.

Selected corporate earnings reports outside the technology sector highlighted divergent fundamental conditions across consumer and manufacturing lines. Ford Motor Co. gained 2.1% after management raised its full-year profit outlook for the second time this year, citing durable demand for commercial fleet vehicles and hybrid powertrains. Visa Inc. rose 0.6% after exceeding consensus earnings targets, supported by strong international transaction volumes linked to global soccer tournament travel demand. In contrast, Lennox International Inc. tumbled 21% after the heating, ventilation, and air conditioning equipment manufacturer revised its annual profit forecast downward due to residential construction headwinds.

Macroeconomic conditions continue to be heavily influenced by external cost shocks and historical rate tightening cycles. After peaking near 9% in mid-2022, inflation moderated following 11 rate increases executed by the Federal Reserve through late 2023. However, disinflation progress has stalled in 2026 as global energy price spikes tied to Middle Eastern geopolitical instability affect consumer transport and logistics channels.

As financial markets look toward late summer, traders are assigning an increased probability to policy action at the Fed’s next scheduled meeting on September 15–16. Prior to that session, market analysts will closely monitor Chair Warsh’s scheduled keynote address at the annual Jackson Hole Economic Symposium in late August for further indicators regarding the central bank’s rate trajectory and balance sheet policy, according to Source Name.

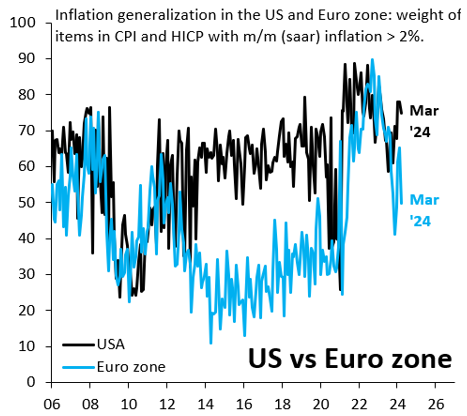

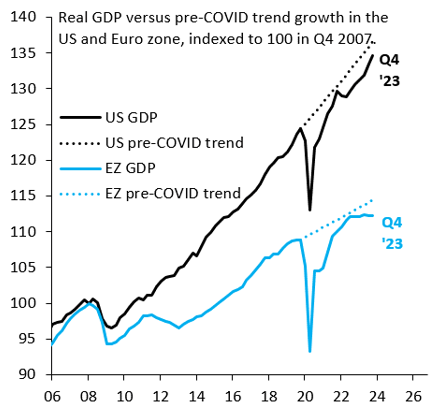

A stylized fact following the 2008 crisis is that U.S. growth substantially outperformed the rest of the advanced world. This again looks to be true in the aftermath of COVID-19 (Figure 1), with lots of debate on the underlying drivers. Some argue that this outperformance reflects loose fiscal policy and rapid immigration, while others see a productivity boom linked to tight labor markets. Whatever the source, cyclical outperformance may keep U.S. inflation stickier than elsewhere. There are some signs of this. Figure 2 shows the combined weight of items in the U.S. consumer price index (CPI) with month-over-month inflation above 2% (on a seasonally adjusted, annualized basis), alongside the same measure for the eurozone’s harmonized index of consumer prices (HICP). This metric is noisier than if we used year-over-year inflation, but it has the advantage of focusing on recent inflation dynamics, since there are no base effects to muddy the picture. Elevated inflation remains relatively broad-based in the U.S., consistent with strong growth, while inflation momentum is clearly fading in the eurozone.

A stylized fact following the 2008 crisis is that U.S. growth substantially outperformed the rest of the advanced world. This again looks to be true in the aftermath of COVID-19 (Figure 1), with lots of debate on the underlying drivers. Some argue that this outperformance reflects loose fiscal policy and rapid immigration, while others see a productivity boom linked to tight labor markets. Whatever the source, cyclical outperformance may keep U.S. inflation stickier than elsewhere. There are some signs of this. Figure 2 shows the combined weight of items in the U.S. consumer price index (CPI) with month-over-month inflation above 2% (on a seasonally adjusted, annualized basis), alongside the same measure for the eurozone’s harmonized index of consumer prices (HICP). This metric is noisier than if we used year-over-year inflation, but it has the advantage of focusing on recent inflation dynamics, since there are no base effects to muddy the picture. Elevated inflation remains relatively broad-based in the U.S., consistent with strong growth, while inflation momentum is clearly fading in the eurozone.