Spirit Airlines has ceased operations following unsuccessful bailout negotiations, citing rising fuel costs and financial challenges exacerbated by geopolitical tensions.

Spirit Airlines has announced the immediate cessation of its operations after failing to secure a government bailout. The airline’s decision comes in response to a sharp increase in oil prices, which has significantly impacted its operational costs amid ongoing geopolitical tensions.

On Saturday, Spirit Airlines revealed that it has begun the process of shutting down its operations. The airline’s parent company, Spirit Aviation Holdings, confirmed the cancellation of all flights and advised customers who purchased tickets not to go to the airport. Refunds will be processed automatically for those who paid with credit or debit cards, but the company will not assist customers in rebooking through other airlines.

In a statement, Spirit President and CEO Dave Davis expressed his disappointment over the situation. He stated, “The sudden and sustained rise in fuel prices in recent weeks ultimately has left us with no alternative but to pursue an orderly wind-down of the Company. Sustaining the business required hundreds of millions of additional dollars of liquidity that Spirit simply does not have and could not procure.” Davis acknowledged the efforts made by the Trump administration to facilitate a bailout, adding, “This is tremendously disappointing and not the outcome any of us wanted.”

In response to the airline’s closure, Transportation Secretary Sean Duffy announced measures to assist Spirit’s customers. Airlines will cap ticket prices for Spirit passengers seeking to rebook their canceled flights. Additionally, travel benefits will be extended to Spirit employees returning home, ensuring they have available seats on other airlines.

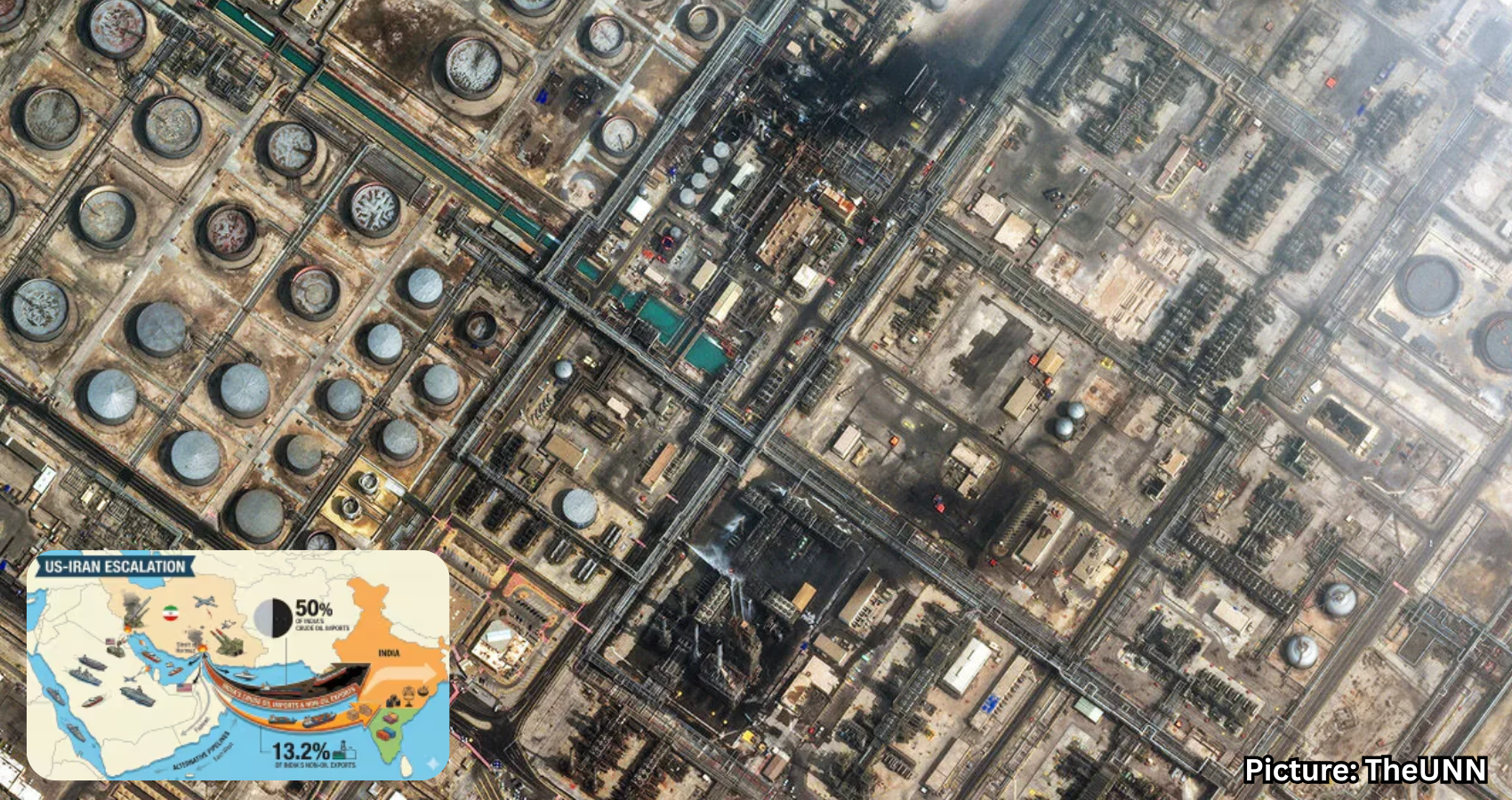

The recent spike in fuel prices has been attributed to ongoing tensions in the Middle East, particularly the conflict involving Israel and Iran, which has affected oil exports through the Strait of Hormuz. These rising costs have posed significant challenges to the airline industry, which has struggled to recover from the financial impacts of the COVID-19 pandemic.

On Friday, President Trump indicated that the administration was considering a government bailout to keep Spirit operational, estimating potential assistance at around $500 million. He emphasized the importance of negotiating a favorable deal, stating, “It’s something we’re not looking to get involved with but, if we can, it’s 14,000 jobs –– I would say we are driving a tough deal but it’s one of those things.” Trump had previously suggested the possibility of a taxpayer takeover of Spirit Airlines, with plans to resell the airline once oil prices stabilize.

The International Association of Machinists and Aerospace Workers (IAM), which represents Spirit employees, expressed concern over the implications of any federal relief. The union stated that any support must ensure protection against layoffs and furloughs, emphasizing that the workers did not cause the airline’s financial troubles. IAM’s statement underscored corporate mismanagement and poor financial stewardship as central issues, declaring, “Today’s news is devastating for the thousands of airline workers who showed up every day and gave everything to keep Spirit Airlines in the air.” The union vowed to hold responsible parties accountable and ensure that workers are not left to bear the consequences of the airline’s failure.

Spirit Airlines has faced significant financial challenges in recent years, reporting losses of more than $25 billion since the onset of the COVID-19 pandemic. The airline filed for Chapter 11 bankruptcy protection in November 2024 amid growing debt and rising operating expenses. The current situation highlights ongoing vulnerabilities in the airline sector, particularly as companies navigate recovery from the pandemic.

Conservative lawmakers have voiced opposition to a government bailout, arguing that taxpayer funds should not be used to support failing businesses. Senator Tom Cotton (R-Ark.) labeled the proposed bailout as “not the best use of taxpayer dollars,” while Senator Mike Lee (R-Utah) cautioned that such assistance could undermine competition in the airline industry, stating that bailouts risk creating a precedent that could harm market dynamics.

The closure of Spirit Airlines marks a significant event in the ongoing saga of the airline industry’s recovery and raises questions about the long-term viability of low-cost carriers in the face of rising operational costs. As the industry grapples with these challenges, the need for sustainable business practices and government support frameworks will become increasingly critical, according to Source Name.